Is AeroVironment Stock a Buy, Sell, or Hold for September 2025?

Defense stock AeroVironment (AVAV) has been surging this year on the back of solid results and underlying operational prowess. CNBC’s “Mad Money” host Jim Cramer has even compared the stock to defense technology supergiant Palantir Technologies (PLTR), calling it the “Palantir of Hardware.”

Cramer believes this high-flying stock could become a powerful long-term wealth creator, much like Palantir.

But more recently, shares have stalled in their rally, down nearly 10% over the past month. What should you do with AeroVironment now?

About AeroVironment Stock

Founded in 1971 and headquartered in Arlington, Virginia, AeroVironment specializes in unmanned aircraft systems (UAS), tactical missile systems, and robotic technologies. The company is a well-established name in the aerospace industry, designing and developing advanced solutions for both military and commercial applications.

AeroVironment’s Raven, Puma, and Wasp series of products are widely used by defense forces worldwide. The company’s focus has always been on small, versatile, and efficient systems that deliver cutting-edge technologies for surveillance, reconnaissance, and payload delivery.

With a market capitalization of approximately $12.4 billion, AeroVironment remains a solid performer on Wall Street despite its latest selloff. The stock has gained 25% over the past 52 weeks. This year, the stock has increased by 60%. It reached a 52-week high of $295.90 in June, but is down 18% from this high.

High-flying stocks like AeroVironment often command premium valuations, and this one’s no exception. Trading at a steep 76.6 times forward earnings, the stock is priced far above the sector median of 23x.

AeroVironment Soars After Q4 Earnings Results

Following AeroVironment’s knockout fourth quarter results, released on June 24, which sailed past both Wall Street’s top and bottom line forecasts, the stock took off almost 21.6% in the very next trading session as investors cheered the strong finish to fiscal 2025. The company reported record quarterly revenue of $275.1 million, indicating a 40% year-over-year (YOY) growth. This is also higher than the $242 million figure expected by Wall Street analysts.

For the fiscal year, AeroVironment reported record bookings of $1.2 billion, which creates a sound pipeline for generating future revenue. Management pointed out investments in its multi-generational Uncrewed Systems and Loitering Munition Systems products as a reason for this gain.

As of Apr. 30, the company also reported a solid backlog of $726.6 million, as compared to $400.2 million as of the prior-year’s period. Funded backlog is defined as remaining performance obligations for which funding has been or is currently appropriated under a customer contract.

On this top line, AeroVironment reported solid quarterly adjusted EBITDA of $61.6 million, nearly triple the amount it was a year ago. It generated an adjusted EPS of $1.61, representing a whopping 274% YOY increase. The reported EPS also surpassed analysts’ consensus estimate of $1.38.

For fiscal year 2026, the company expects revenue in the range of $1.9 billion to $2 billion, non-GAAP adjusted EBITDA of $300 million to $320 million, and non-GAAP EPS in the range of $2.80 to $3. The forecast figures also take into account the impact of AeroVironment’s acquisition of BlueHalo, LLC. The new entity, created after this transaction, is called AV. Its offerings include autonomous uncrewed systems, precision strike, and defensive systems.

Other factors include multiple contracts that the company has signed with the defense forces of various countries, as well as a series of product launches, including the Counter-Unmanned Aerial Systems (C-UAS) technology Titan 4 and tactical autonomy-focused UAS Red Dragon.

What Do Analysts Think About AeroVironment Stock?

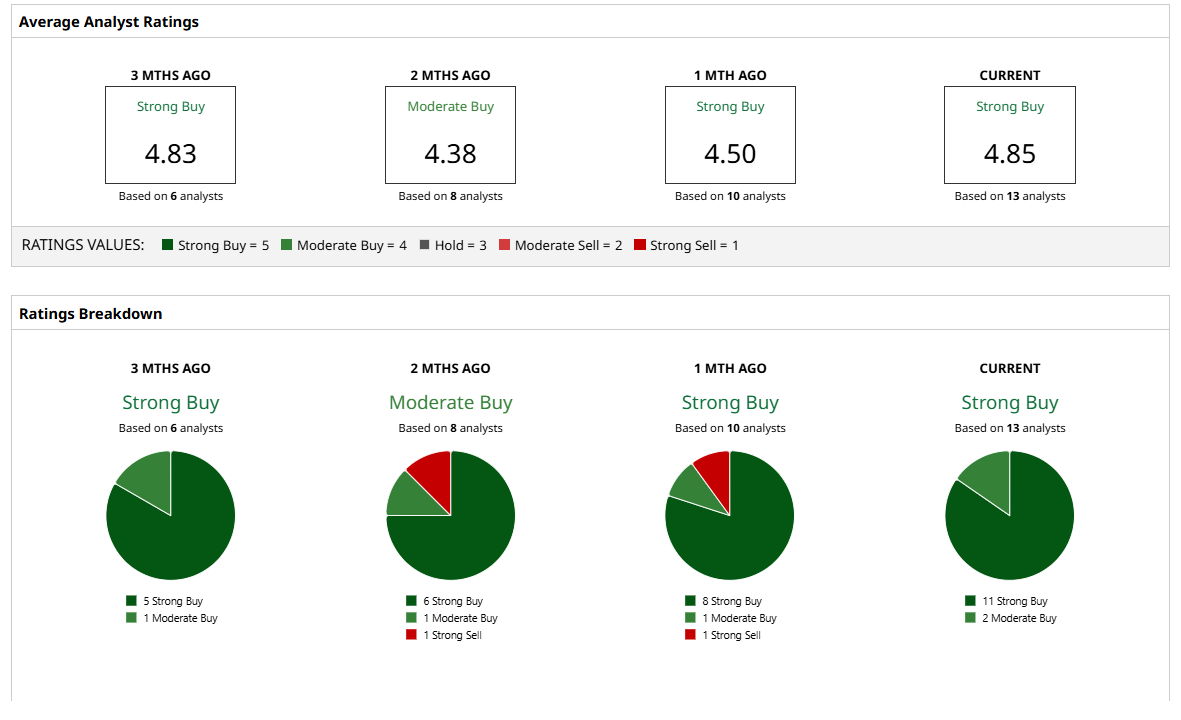

Analysts are particularly keen on AeroVironment stock, assigning it a consensus rating of “Strong Buy.” Of the 13 analysts rating the stock, 11 have assigned it a “Strong Buy” rating and two recommend a “Moderate Buy” rating. The consensus price target of $297.33 represents 23% upside potential. The Street-high price target of $335 implies nearly 40% upside.

Key Takeaways

AeroVironment’s recent growth has been promising, earning the company the support of Wall Street analysts. While the company has a long way to go before it becomes as prominent as Palantir in its own field, AeroVironment might be a solid investment choice now, as the bullish case shows that the stock still has room to grow. Moreover, the company has touted its ability to be useful for President Donald Trump’s “Golden Dome” missile defense system project. This $175 billion project is expected to be operational in approximately three years.

On the date of publication, Anushka Mukherji did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.